December 29, 2022 – By Nick Plasencia

Review and download the PDF version of Hospitality Industry Insights – In High Demand: Florida Hotels and Resorts (Again)

In an article we published in February 2021, before the COVID-19 vaccines were broadly rolled out, we suggested to owners of hotels in Florida, and waterfront hotels in the Sunshine State in particular, that their assets would soon be in high demand.

In the nearly two years since, new pricing records have dotted the Florida peninsula, from the Panhandle to the Keys, Tampa Bay to Jacksonville, and Orlando to South Beach. Investors have flocked to the seemingly bulletproof fundamentals of Florida’s hotel industry. While healthy deals inked in the late spring and summer 2022 have found their way to the finish line, the hotel transaction market nationally has been upended in the last half of this year by turmoil in the debt markets and fears about a looming recession. What then, is the near-term prognosis for the transaction market and asset values in Florida?

As our colleague, Dexter Wood, so clearly articulated this past August in his “Hotel Debt Quagmire” piece, lower loan-to-value ratios, coupled with higher interest rates, have wreaked havoc on underwriting metrics, placing many owners with impending debt maturities in a precarious position. These very same debt dynamics are plaguing the hotel transaction market today. By and large, would-be buyers are challenged to procure debt proceeds of sufficient size and at an attractive enough cost to make sense of the asking price of hotels on the market.

Furthermore, recession concerns have left many investors skeptical about growth in their five-year operating proformas, the backbone of their underwriting. Lower NOI growth and expanding exit cap rates, layered on top of the debt market turmoil, have proven challenging to say the least.

The lodging sector currently finds itself at an inflection point in the marketplace, with most would-be sellers of high-quality assets unwilling to part with their properties at valuations that are more reflective of the current capital market dynamics than the underlying durability of their cash flows and the irreplaceability of their real estate. Transaction activity has accordingly contracted considerably. The outlook for Florida, however, is not as bleak. Current debt markets aside, the lodging fundamentals and outlook throughout the state have never been stronger. Record tourism coupled with resurgent corporate and group demand have created a new normal that far surpasses all pre-pandemic benchmarks for the state. With a bit of patience, Florida hotel and resort owners will continue to reap the rewards of their investments.

Florida in Focus

As has been widely chronicled, Florida has been the domestic darling of the pandemic era. Net migration to the state has led the U.S., at the expense of major metropolises across the Northeast, Midwest, and West Coast. New business applications have surged, and there has been a tangible positive shift in the state’s economy. Major corporations have opened new offices in the state or altogether relocated to Florida. The mild weather and absence of a state income tax have also made Florida a refuge for an army of fully remote employees who have turned the traditional vacation destination into an everyday oasis.

Domestic inbound travel to Florida has surpassed prior peaks, and international travel is returning to pre-pandemic norms, albeit very slowly, but nevertheless providing additional support for future RevPAR increases. In 2019, international visitation comprised some 11% of all travelers to the state. Due in large part to an unfavorable exchange rate, unpredictable travel dynamics, and variances in global pandemic travel restrictions, international visitation to the Sunshine State remains just a fraction of pre-pandemic levels. International visitation in Florida during the September 2022 trailing twelve-month (TTM) period was 41% below 2019, with 5.7 million fewer international travelers in total. The continued natural recovery towards pre-pandemic benchmarks will provide an additional layer of demand to Florida’s hotels.

Rock Solid Fundamentals

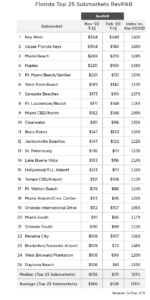

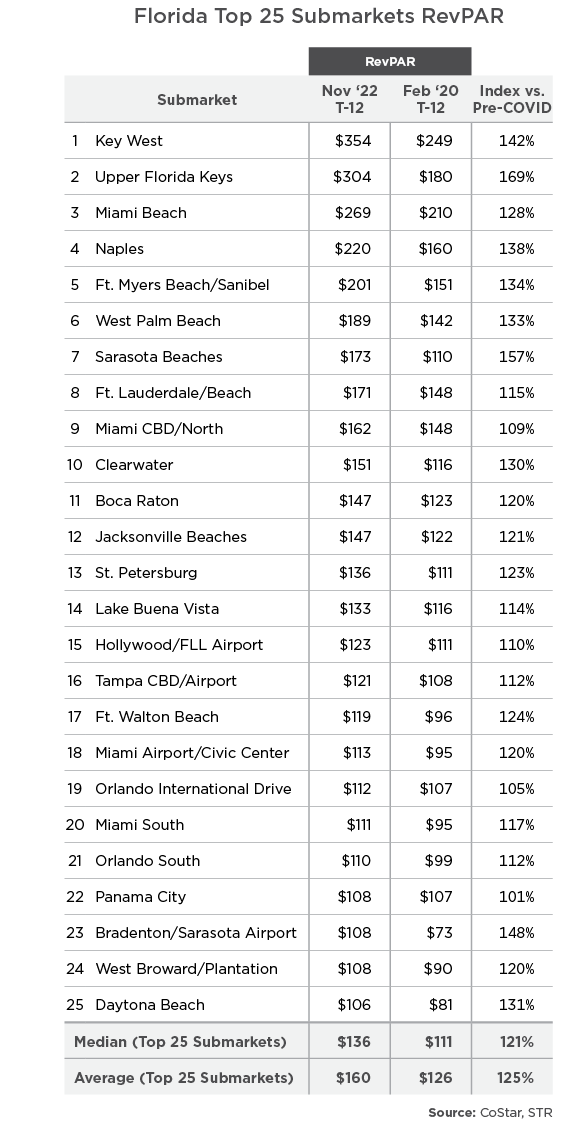

The table at right depicts the RevPAR of Florida’s top 25 submarkets, as tracked by STR. The improvements in hotel performance that the state has experienced are remarkable. On a TTM basis, each of these submarkets has surpassed the final, “clean” pre-pandemic TTM period ending February 2020. Unsurprisingly, most of this growth has been driven by ADR during this inflationary period (median submarket TTM ADR is 28% higher than pre-pandemic) while demand has been remarkably strong, with the median submarket Occupancy in the state now only slightly below pre-pandemic figures. For group- and corporate-anchored submarkets such as Orlando’s and Tampa’s Central Business District, respectively, recent performance has been supercharged as those demand segments have returned.

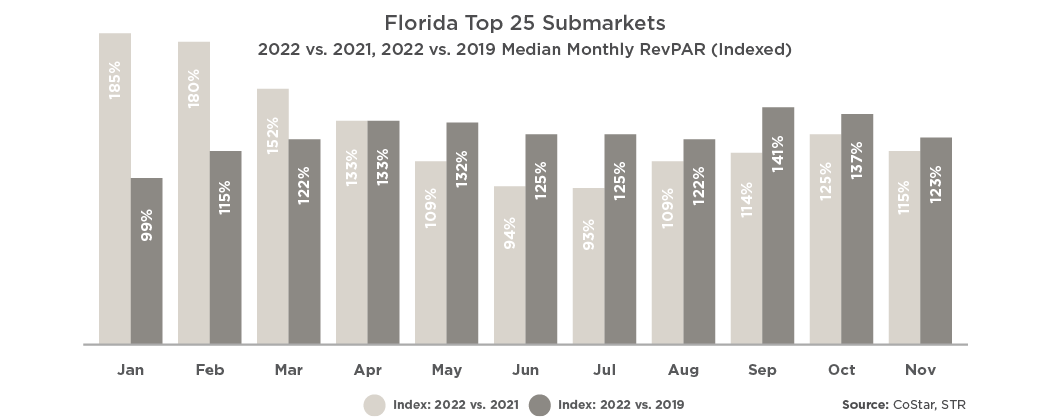

For the past year, we’ve heard concerns from investors that the euphoric run-up in performance experienced in summer 2021 at the end of many pandemic restrictions might be unsustainable. Travelers with cabin fever and, more importantly, cash in their bank accounts, flocked to Florida in record numbers, resulting in record ADRs. The numbers this year bear out some of these concerns, but actually paint a rosier picture than many initially feared. Top beach markets across the state did indeed experience a notable year-over-year decline in RevPAR in June and July 2022, leading to median RevPAR declines across these 25 markets of 6% and 7% in those months, respectively. These declines, however, moderated significantly by late summer, and August once again proved to be an excellent month of year-over-year growth in most submarkets. While September and November figures were undoubtedly distorted by Hurricanes Ian and Nicole, the numbers across the balance of the state largely continued to improve this fall. For group- and corporate-anchored submarkets such as Orlando and Tampa’s Central Business District, recent monthly performance has been supercharged as those demand segments have returned.

Looking ahead, we believe owners of Florida hotels and resorts can rely on 2022 being a sturdy baseline for projecting future performance — and don’t forget that travel in January 2022 was meaningfully impacted by the COVID Omicron variant! We anticipate that Florida hotel and resort performance in 2023 should handily surpass 2022 in the vast majority of cases, rooted in tenacious leisure travel, diminished COVID concerns, and consistently expanding corporate and group demand.

Patience has Paid Off

While current conditions have created a tenuous investment market for most hotel assets nationally, the amount of equity capital seeking superior hotels remains exceedingly high, and quality opportunities are being duly scrutinized. The United States stands out as a global safe haven today, beckoning capital from every corner of the planet, and Florida has become the most attractive part of the nation for lodging investments. Most owners in the Sunshine State who have been warily eyeing transaction trends will find that an on-market or discreet, off-market disposition outreach effort today will likely yield considerable interest, notwithstanding the current economic environment.

For many of our clients, patience has proven to be the prudent approach over the last four or five months. Current economic woes, however, will not last forever. As when the debt markets reopened in early 2021, lenders dipping their toe back into the lodging sector will be looking for security above all else. Few economies in the country and world are as strong as Florida’s, and we expect loan originations in the state will again become a top priority for lenders with allocations to the hotel sector.

Florida also has been unfairly dinged this year by a prevailing sentiment that the rush of leisure demand into the state in 2021 was nothing but a stimulus-induced “sugar high,” not to be replicated. While many top beach destinations did suffer moderate year-over-year declines in RevPAR over the course of the early summer, most coastal destinations quickly stabilized. The state appears to be settling into a new normal era of heavy leisure demand, buoyed by increases in corporate and group business segments, as well as improving international travel.

To the many would-be sellers of hotels and resorts in Florida: you once again might be surprised by how voracious investors’ appetite for your properties may be today. The public lodging REITs, flush with cash and not constrained by property-level mortgage underwriting, have thrown their weight around during the second half of 2022, paying fair values for leisure assets across the country. Private equity, high-net-worth family offices, and institutional investors have taken notice. With budget season behind us, there is every reason to believe 2023 will be rosier than 2022 for the Florida lodging sector, especially at the top line. Trailing twelve-month performance will swell as tourists flock to the Sunshine State this winter and spring and Omicron disruptions roll off the books. You can bank on investor capital chasing closely behind. As the capital markets emerge from their hibernation, Florida remains right where it has been for the last two years: at the top of the list for every investor and lender.

For more valuable hospitality industry news and market analysis from The Plasencia Group, be sure to opt-in to our news and communications list.